The Business of Wine: Opus One Winery

May 1, 2014Interview: Concierge Services

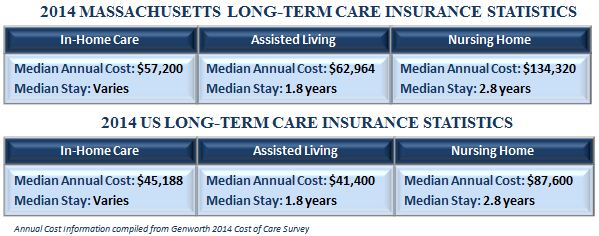

May 20, 2014Long-Term Care Insurance

With an aging population and longer life expectancies, caring for an older family member can be a strain on a family, both financially and emotionally. We think about the quality of life we want to live in retirement as we do our best to make our aging family members comfortable and their final years enjoyable.

We hope and plan to live our lives as independently as possible and not become a financial burden on our loved ones, but around-the-clock care is time consuming and expensive. Along with planning for an independent and financially secure retirement, planning for late in life care is essential.

Ideally, financial planning for long-term care should occur long before the need arises. The majority of people over age 65 (70 percent) will require some type of long-term care services during their lifetime, and over 40 percent will need a period of care in a nursing home.1 Fortunately, there are steps you can take—whether a nursing home is needed now, next month or next decade—to minimize the strain.

LTCI Basics

Long-term care insurance (LTCI) helps pay for medical expenses associated with home care, assisted living, and nursing homes. Although the future isn’t foreseeable, being prepared can help to combat out of pocket expenses and protect your assets. Whether considering a policy for yourself or for a family member, it is necessary to take into consideration many factors when purchasing a long-term care insurance policy. Selecting a policy should be based on a careful evaluation of your net worth, your health, and your wishes.

When to Purchase LTCI

The cost of long term care insurance is contingent upon your age, health and the type of policy you purchase. Purchasing a policy in your 40’s vs your 50’s or 60’s drastically decreases the total premiums paid over time.

Each year you wait to buy a policy, on average insurers increase premiums by 3% to 4%, according to the American Association for Long-Term Care Insurance.2